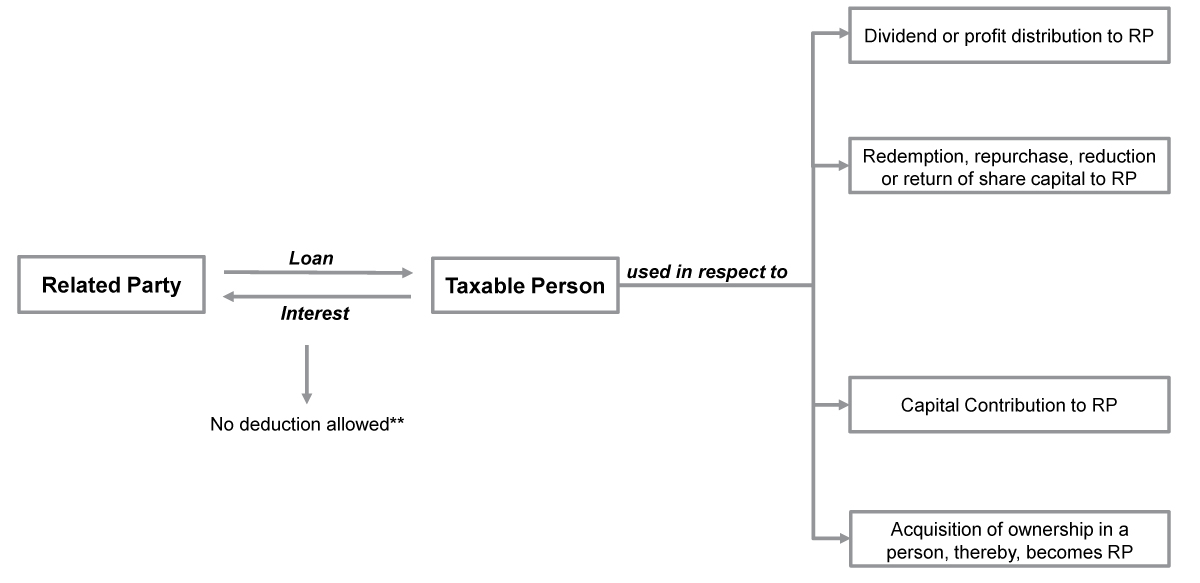

** exception : main purpose for obtaining the loan is not to gain corporate tax advantage

No Corporate Tax Advantage mean where related party is subject to corporate tax or tax of similar character on interest in foreign jurisdiction is not less 9% as provided under para (b) of clause 1 of Article 3 of this Decree.-law